As organizations enter 2026 planning cycles, internal audit teams are facing a pivotal moment. Pressures from regulation, technology modernization, and shifting risk landscapes are reshaping expectations of what audit functions deliver and how they provide it. The traditional audit model, built around cyclical reviews and backward-looking assurance, is giving way to a more dynamic, data-driven approach focused on real-time insight and strategic value.

Here are two significant trends defining the transformation of internal audit programs and what forward-thinking teams should be prioritizing for 2026.

1. Continuous Risk Monitoring Is Becoming the New Baseline

The days of static audit plans are over. In leading institutions, continuous risk monitoring has evolved from a pilot initiative into a central design principle. By integrating live data streams from finance, operations, and compliance systems, audit teams can now continuously assess exposure and trigger reviews based on emerging risk signals, rather than relying on fixed calendars.

This shift is powered by data analytics and automation, but a mindset change drives it: auditors are moving from reporting on what happened to explaining what’s happening.

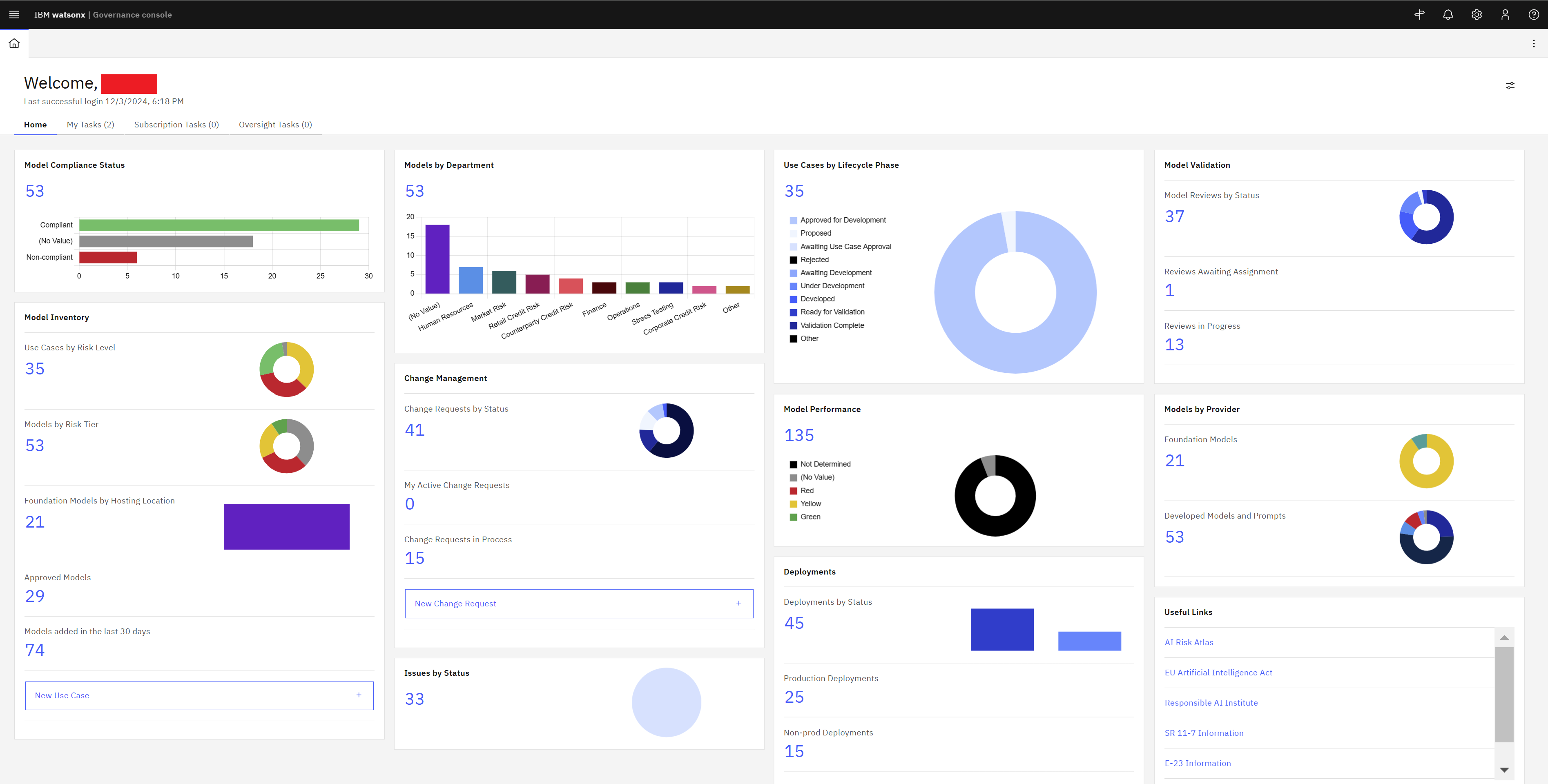

For many teams, this means rethinking their audit universe entirely, mapping risks to data sources, aligning with the organization’s enterprise risk taxonomy, and using technology platforms like IBM OpenPages or SAS Viya to feed key risk indicators (KRIs) directly into the audit workflow.

What to do for 2026:

Develop a “living audit plan” model that’s refreshed quarterly based on data triggers, rather than solely on management input. Start small with high-risk areas like third-party management or IT change control, then scale.

2. Audit Is Moving Closer to Assurance of Controls, Not Just Testing Them

Another major shift is the move toward control assurance integration, where audit plays a proactive role in validating control design and performance throughout the year. Instead of relying on manual sampling, leading teams are leveraging control analytics, robotic process automation (RPA), and AI-assisted testing to evaluate whether controls are operating effectively continuously.

This creates a tighter alignment with second-line functions, especially Compliance and Risk, resulting in a unified control assurance view that strengthens both governance and efficiency.

For 2026, expect to see more audit programs investing in control testing automation within GRC platforms and deploying analytics to test entire data populations, not samples.

What to do for 2026:

Map your control library to data sources and identify where automated testing can be embedded. Focus first on operational and IT general controls areas where automation yields immediate credibility gains with regulators and executives.

Looking Ahead

The number of audits delivered won’t define the internal audit function of 2026; it will be determined by the clarity and foresight it provides to management and boards. Teams that invest now in data integration, automation, and collaboration across the three lines will emerge as strategic enablers rather than reactive reviewers.

.webp)

-1.jpg)

.jpg)

.jpeg)